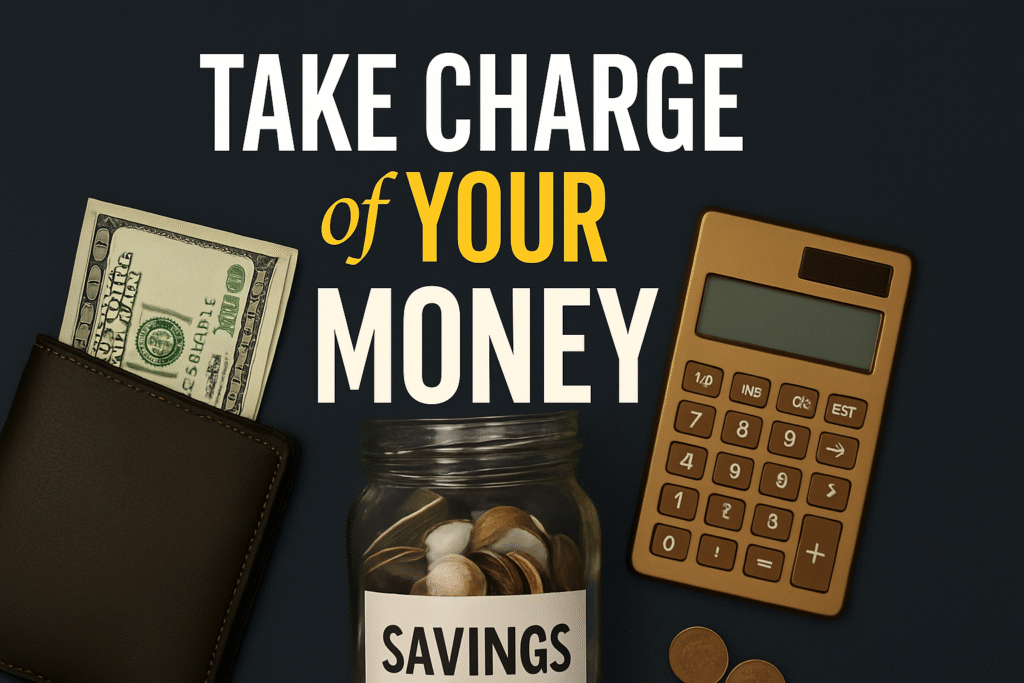

Money management simply means how you handle your income — how much you spend, save, and invest. It’s about being smart with your money, setting goals, and making sure you’re financially secure now and in the future.

Just earning more won’t make you rich. If you don’t know how to manage your money, it can vanish quickly. Spending all your income might feel fun now, but without planning, you’ll struggle later. This would help emotionally connect the reader. That’s where money management helps, it gives you control over your finances and peace of mind.

Think money management is tough? Don’t worry. In this blog, I’ll break down smart, easy ways to handle your money, so you can enjoy the present without stressing about the future.

Some Core Pillars of Money Mastery — Build Your Financial Future Right:

Budgeting:

Creating a budget is the first and most powerful step toward gaining control over your finances. One of the simplest and most effective budgeting methods you can follow is the 50/30/20 rule a popular strategy introduced by U.S. Senator and financial expert Elizabeth Warren, along with her daughter Amelia Warren Tyagi, in their 2005 book All Your Worth. According to this rule, you divide your monthly income into three clear categories: 50% for needs, 30% for wants, and 20% for savings and debt repayment.

The first 50% covers your essentials things like house rent, property tax, utility bills such as electricity and water bills, daily transportation costs (like fuel or public transport), and school or college fees. These are the non-negotiable expenses; these expenses keep your life running smoothly. The next 30% is for your wants, things that make life enjoyable but aren’t strictly necessary. This could include branded clothes and shoes, dining at fancy restaurants, ordering food online, or upgrading to the latest smartphone. Lastly, the remaining 20% should be set aside for saving and debt repayment. This portion helps you build an emergency fund, invest in your future, or pay off any existing loans or credit card dues.

Tracking your Expense:

Start by tracking your expenses. It is all about where your money goes. You can do this by writing down in a notebook, use an Excel sheet, or try one of the budgeting apps available today. The goal is to maintain a clear record of your spending, whether it’s daily, weekly, or monthly. This helps you stay aware of your financial habits and ensures that your budget stays on track. Tracking brings transparency to your financial habits and helps you understand exactly where your money is going. Once you’re aware of your spending patterns, it becomes easier to adjust and stick to your budget. This simple habit not only helps you avoid overspending but also puts you on the path to financial stability and achieving your long-term financial goals.

Start Saving:

Saving means keeping some part of your income instead of spending all of it. It helps you get ready for future needs like emergencies, retirement, or big goals such as buying a car or a house. Saving gives you peace of mind and makes you feel more comfortable about your future. As the saying goes, “Saving is not about how much you earn, it’s about how wisely you keep or spend what you have. A little today can become your freedom tomorrow.” Even small savings today can make a big difference in your future.

Investment:

Investing is all about putting your money into things that can grow in value over time. Instead of keeping all your money in savings, it’s a smart idea to use a portion of it to invest in assets like stocks, mutual funds, real estate, fixed deposits, or even gold. These investments can help you build wealth and achieve future goals like buying a house, starting a business, or planning for retirement.

But remember, investment always comes with some risk. That’s why it’s important to learn about the options, understand the risks involved, and only invest a part of your savings, not all of it. The key is to start small, stay informed, and grow your money step by step.

Spending Wisely:

Spending wisely means thinking before you spend and using your money smartly. It’s about asking yourself, “Do I really need this, or am I just buying it for no reason?” When you spend carefully, you make sure your money is going towards things that are useful and important, not just things you want in the moment. Try to avoid impulse spending, buying something just because it looks nice or is on sale. The more mindful you are with your money, the easier it becomes to save and reach your future goals.

.

Build an Emergency Fund:

Building an emergency fund means saving money specifically for unexpected situations. An emergency fund is money you set aside to help you deal with sudden expenses like a medical emergency, job loss, or urgent home repairs. It’s not for shopping or vacations, but for situations where you need quick help. Even if you save a small amount every month, it can give you peace of mind and protect you from financial stress. Think of it as your helping partner during tough times.

Debt Management:

Debt management is the process of planning, organizing, and repaying your borrowed money smartly and responsibly. The first step is to avoid taking loans unless necessary. If you do need a loan, make sure it’s for something that improves your financial future, like starting a business, not for buying expensive clothes, the latest smartphone, or a smart TV that you can’t afford. If you already have debt, focus on repaying high-interest loans first, such as credit cards. Never take a new loan just to pay off an old one; it only creates a cycle that’s hard to escape. Always keep your EMIs within your budget so you can repay them comfortably and live without financial stress. One more important thing — don’t lend money to others if you’re not financially stable yourself. Doing so can lead to stress and weaken your financial position.

Benefits of Money Management:

Helps you control your spending.

Reduces financial stress.

Improves savings and investments.

Keeps you prepared for emergencies.

Helps you achieve financial goals.

Avoids unnecessary debt.

Gives peace of mind and confidence.

Money can either control you or work for you; the choice is yours. When you build good money habits now, you’re setting yourself up for a better future. Whether you’re just starting or trying to improve your finances, remember — even small steps can lead to big changes over time. So, start managing your money today — your future self will thank you.

By Himansh Kumar | June 22, 2025

2 thoughts on “Control Your Money Before It Controls YOU: LIKE a Pro”